Stress testing in banking: key methods and climate risk

Stress testing has always been a cornerstone of banking supervision, but the numbers coming out of recent regulatory exercises should stop risk professionals in their tracks. Climate scenarios alone can drive Common Equity Tier 1 (CET1) capital depletion of 74 to 77 basis points in a single stress cycle, with some sectors facing probability of default (PD) increases of up to 40%. These are not projections from theoretical models. They are outputs from real supervisory programs run by the European Central Bank (ECB) and the Deutsche Bundesbank. For candidates preparing for the GARP Sustainability and Climate Risk (SCR) exam, mastering these frameworks is no longer optional. It is the difference between passing and falling short.

Table of Contents

- What is stress testing in banking?

- Key methodologies and regulatory frameworks

- Climate and environmental risk: hidden catalysts and exam essentials

- Systemic risk, contagion, and scenario design challenges

- A fresh perspective: what most exam-takers (and banks) miss about stress testing

- Advance your climate risk expertise for certification and beyond

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Stress testing essentials | Modern stress testing blends regulatory models with bank-specific data to assess resilience under severe scenarios. |

| Climate risk integration | Transition and physical climate risks are now central, often amplifying capital impact in key industries. |

| Systemic vulnerabilities | Scenario design must account for market contagion, fire sales, and model uncertainty to avoid blind spots. |

| Exam success factors | Understand both mechanical processes and the limitations of current frameworks for top exam performance. |

What is stress testing in banking?

Stress testing is a forward-looking risk management tool that measures how a bank’s capital position would hold up under severely adverse but plausible economic or financial conditions. At its core, the process involves designing hypothetical scenarios, running bank exposures through those scenarios, and projecting the resulting impact on key financial metrics over a defined time horizon.

The regulatory origins of modern stress testing trace back to the post-2008 financial crisis reforms. The Federal Reserve, ECB, Bank of England, and other major supervisors introduced formal stress testing programs to address the systemic failures that the 2008 crisis exposed. In the United States, the Fed’s Dodd-Frank Act Stress Test (DFAST) and the Comprehensive Capital Analysis and Review (CCAR) became the primary vehicles for this oversight. The Fed’s supervisory stress tests use models to project losses, revenues, expenses, and capital under hypothetical severe recession scenarios over a 9 to 13 quarter horizon, incorporating macroeconomic variables like unemployment, gross domestic product (GDP), and house prices.

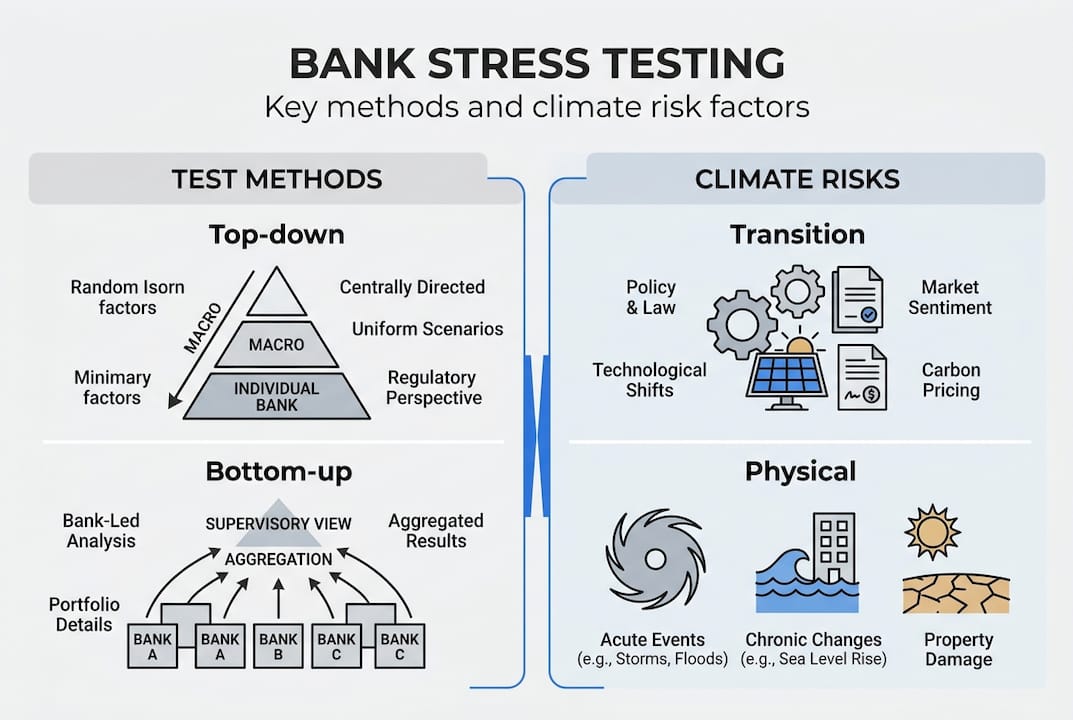

Two broad approaches exist in practice. Top-down stress testing is conducted by regulators using standardized models applied across many institutions simultaneously. It allows consistency and comparability but may miss institution-specific nuances. Bottom-up stress testing is run by individual banks using their own internal models, providing more granularity but requiring rigorous independent validation.

Key metrics that stress tests aim to assess include:

- CET1 ratio depletion: The reduction in the highest-quality capital buffer under stress

- Projected net losses: Including loan losses, trading losses, and operational losses

- Net interest income (NII): How revenues hold up when rates and credit conditions deteriorate

- Tier 1 leverage ratio: A supplementary capital adequacy measure

- Risk-weighted asset (RWA) changes: How credit and market risk profiles shift under stress

For exam candidates exploring how these metrics connect to broader ESG frameworks, the CFA ESG mock exam provides a useful starting point for scenario-based practice.

Pro Tip: Exam questions frequently focus on how scenario design choices, such as the severity of a GDP shock or an unemployment spike, drive different capital outcomes. Understanding the transmission mechanism from scenario variable to capital metric matters far more than memorizing a formula.

| Metric | Description | Why it matters |

|---|---|---|

| CET1 depletion | Capital ratio decline under stress | Core capital adequacy measure |

| Projected losses | Credit, market, operational | Total financial impact |

| NII projection | Revenue sustainability | Profitability under stress |

| RWA changes | Risk-weighted asset evolution | Capital requirement shifts |

Key methodologies and regulatory frameworks

The mechanics of stress testing vary significantly across regulatory regimes, but the underlying model architecture shares common components. Understanding these components is essential both for exam success and for practical application in a banking risk function.

The Federal Reserve’s credit risk models illustrate the level of granularity involved. Fed corporate credit models use BBB spread for PD and loss given default (LGD) projections, and apply a constant 50% loan equivalent factor (LEQ) for exposure at default (EAD) on revolving exposures due to data scarcity. This kind of modeling convention, driven by practical constraints rather than theoretical ideals, is exactly the type of detail that separates a strong exam response from a superficial one.

The ECB’s European Banking Authority (EBA) stress test follows a similar structure but places greater emphasis on static balance sheet assumptions and scenario narratives driven by the European Systemic Risk Board (ESRB). Germany’s Bundesbank has also run sector-specific climate exercises on top of standard macro stress tests, reflecting the increasing integration of sustainability into prudential supervision.

“Stress testing frameworks are only as strong as the scenarios feeding them. When model inputs are constrained by data availability rather than risk reality, the outputs can understate systemic vulnerability.”

The main steps in running a regulatory stress test include:

- Define the scenario: Regulatory authority specifies baseline and adverse paths for macro variables.

- Map exposures: Banks classify assets by type, sector, geography, and risk rating.

- Run credit risk models: Apply PD, LGD, and EAD estimates under stress conditions.

- Project revenues and expenses: Model NII, fee income, and operational costs under the scenario.

- Calculate capital impact: Aggregate losses and revenue changes to project CET1 ratios.

- Compare against thresholds: Assess whether the bank remains above minimum capital requirements.

- Report and remediate: Publish results or use them internally to strengthen capital planning.

| Framework | Regulator | Approach | Climate integration |

|---|---|---|---|

| DFAST/CCAR | Federal Reserve | Top-down and bottom-up | Emerging |

| EBA stress test | EBA/ESRB | Bottom-up, static balance sheet | Partial, via extensions |

| Bundesbank climate test | Deutsche Bundesbank | Sector-specific, physical and transition | Full integration |

| ECB SREP | ECB | Institution-specific, ICAAP-based | Increasing |

Candidates preparing for GARP SCR exam strategies should pay close attention to the differences between these frameworks, particularly regarding static versus dynamic balance sheet assumptions and how each treats contagion effects.

Climate and environmental risk: hidden catalysts and exam essentials

The integration of climate risk into bank stress testing represents the most significant methodological shift in prudential supervision since the 2008 reforms. Climate risk introduces two distinct transmission channels that require different modeling approaches: transition risk and physical risk.

Transition risk arises from the economic disruption of moving to a low-carbon economy. Policy changes, such as carbon pricing, new regulations, and shifts in technology preferences, can rapidly alter the creditworthiness of carbon-intensive borrowers. The German Bundesbank’s climate stress test provides some of the clearest empirical evidence: an abrupt CO2 price increase of 200 euros per tonne raises PDs by up to 40% for non-financial corporates after three years, with the most severe impacts concentrated in agriculture, utilities, and transport sectors.

Physical risk encompasses both acute events, such as floods and wildfires, and chronic changes, such as sea-level rise and shifting precipitation patterns. These risks translate into direct asset damage, supply chain disruption, and broader macroeconomic slowdown. The 2025 EU-wide stress test found that transition risks from green investments add approximately 74 basis points of CET1 depletion, while acute physical risks from events like floods add around 77 basis points through direct damage, local disruptions, and macro spillovers.

Key sectors to understand for exam purposes include:

- Agriculture: High sensitivity to temperature, drought, and flood risk; transition costs from fertilizer and energy price changes

- Utilities: Stranded asset risk from fossil fuel infrastructure; capital expenditure requirements for renewable transition

- Transport: Exposure to carbon taxes, fuel cost shocks, and fleet electrification costs

- Real estate: Collateral value at risk from physical damage and energy efficiency regulations

Pro Tip: Exam questions on climate stress testing often require candidates to trace the transmission channel from a climate event or policy change through to a specific capital impact. Practice mapping: climate shock, then borrower PD change, then bank loss, then CET1 depletion. Understanding these climate transition risks in sequence builds the analytical clarity examiners reward.

The ECB’s climate risk framework also emphasizes the role of climate risk externalities that markets frequently fail to price correctly, making regulatory intervention through stress testing a critical correction mechanism.

| Climate risk type | Scenario driver | Affected sectors | CET1 impact |

|---|---|---|---|

| Transition (orderly) | Gradual CO2 pricing to 2050 | Energy, utilities | Moderate |

| Transition (abrupt) | €200/t CO2 price shock | Agriculture, transport | Up to 40% PD increase |

| Physical (acute) | Flood events | Real estate, agriculture | ~77 bps CET1 depletion |

| Physical (chronic) | Sea-level rise, heat stress | Coastal real estate | Long-term collateral erosion |

The GARP SCR climate course covers these transmission mechanisms in structured detail, aligning with the specific weighting the SCR exam places on climate risk integration into financial analysis.

Systemic risk, contagion, and scenario design challenges

Even the most sophisticated bank-level stress test captures only part of the picture. Systemic risk, the risk that stress in one institution or market amplifies across the entire financial system, requires a different analytical lens. This is where contagion modeling becomes critical.

Contagion in banking stress tests operates through several well-documented channels. Fire sales occur when stressed banks liquidate assets rapidly, driving prices down and creating mark-to-market losses for other holders of the same assets. Fund holdings create second-round effects, as investment fund redemptions force asset sales that feed back into bank balance sheets. Counterparty defaults generate direct credit losses and indirect liquidity pressures across interconnected networks.

The 2025 EU-wide stress test quantified these effects with notable precision. System-wide contagion analysis found that fire sales and fund holdings add 29 basis points of CET1 depletion on top of institution-specific losses, with equity funds hit hardest and banks with poor hedging positions facing the greatest amplification of losses.

“The gap between bank-level and system-level stress test outcomes reveals how much risk remains invisible when institutions are analyzed in isolation.”

Several practical barriers complicate effective systemic scenario design:

- Scenario flexibility versus realism: The Federal Reserve’s Global Market Shock (GMS) component lacks constraints on primary risk factors, allowing arbitrary severity levels that may not reflect economically coherent conditions.

- Non-bank financial institution (NBFI) linkages: Shadow banking channels, including money market funds and hedge funds, transmit liquidity shocks that traditional bank stress tests underweight.

- Data availability: Cross-border exposure data, particularly for derivatives and securities financing, remains incomplete in most jurisdictions.

- Behavioral assumptions: Static balance sheet assumptions ignore strategic responses like deleveraging or raising new capital that would realistically occur during a stress event.

For exam candidates, the practical implication is to expect questions that ask about the limitations of stress test frameworks, not just their mechanics. Understanding what a model cannot capture is as important as knowing what it can.

Relevant internal resources for deeper study include climate risk disclosure and climate risk management strategies, both of which connect stress test outcomes to broader risk governance frameworks.

| Contagion mechanism | Transmission channel | Impact magnitude | Mitigation |

|---|---|---|---|

| Fire sales | Asset price depression | 29 bps additional CET1 loss | Diversified portfolios, limits |

| Fund redemptions | Forced asset liquidation | Amplifies equity fund losses | Liquidity buffers |

| Counterparty default | Direct credit loss | Institution-specific | Collateral management |

| NBFI liquidity shock | Funding market seizure | Systemic | Regulatory oversight |

A fresh perspective: what most exam-takers (and banks) miss about stress testing

The most common mistake in stress test preparation, whether for an exam or in professional practice, is treating the exercise as a technical modeling problem with a single correct answer. It is not. Stress testing is fundamentally an exercise in structured judgment under uncertainty.

The empirical evidence on CET1 impacts across institutions shows heterogeneity ranging from 0.7% to 4.8%, and critics consistently highlight model uncertainty, the absence of true tail risks, and the limitations of scenario narratives that are designed for plausibility rather than worst-case accuracy. Off-the-shelf scenarios, regardless of how rigorous they appear, are backward-looking constructs dressed in forward-looking language.

What deeper practitioners understand is that reverse stress testing, working backward from a failure outcome to identify the conditions that would cause it, provides far more actionable insight than standard forward-looking exercises. It forces a focus on genuine vulnerabilities rather than on whether the institution passes a regulatory threshold. Exam candidates who can articulate the logic of reverse stress testing, and explain why it supplements rather than replaces standard scenarios, consistently produce stronger answers on advanced climate risk techniques.

Pro Tip: When an exam question asks about stress test limitations, bring in reverse stress testing as a constructive alternative. Examiners reward responses that demonstrate awareness of what standard models miss.

Advance your climate risk expertise for certification and beyond

The depth of knowledge required to master stress testing frameworks, from regulatory mechanics to climate scenario design and systemic contagion modeling, reflects the growing complexity of the sustainability and risk management landscape. Banking risk professionals who can demonstrate this expertise hold a clear advantage in both certification outcomes and career progression.

Green Risk Education provides structured, syllabus-aligned preparation for the GARP SCR and CFA ESG courses that cover these frameworks with the precision and depth that exams demand. Whether the priority is SCR exam prep focused on climate risk integration or CFA ESG exam prep for sustainable investing, the platform’s expert-designed resources connect regulatory detail to practical application. Professionals who invest in structured preparation are better positioned to demonstrate credible expertise when it matters most.

Frequently asked questions

What is the main purpose of stress testing in banking?

Stress testing finds vulnerabilities by modeling bank losses and capital sufficiency under severe but plausible macroeconomic or climate scenarios. The Federal Reserve’s supervisory stress tests project losses, revenues, expenses, and capital under hypothetical severe recession conditions to assess whether banks can absorb shocks.

How does climate risk affect bank stress tests in 2026?

Climate risks add both transition and physical loss channels, often increasing capital depletion in affected sectors like utilities, agriculture, and transport. The German banking climate stress test found CO2 price increases raise PDs by up to 40% for non-financial corporates in the most exposed sectors.

What are common pitfalls in modeling stress tests for exams?

Overreliance on static models and ignoring data uncertainty can lead to underestimating systemic or climate-related tail risks. Critics consistently recommend reverse stress testing as a more objective complement to standard forward-looking scenario analysis.

Which metrics measure stress test outcomes?

Common metrics include CET1 depletion, loss ratios, and projected default rates under scenario extremes. The ECB’s stress test extensions use CET1 depletion as the primary summary measure of climate and systemic risk impact.

What is reverse stress testing and why is it important?

Reverse stress testing starts from bank failure and works backward to identify the conditions that would cause it, making it a more targeted tool for exposing genuine vulnerabilities. Industry critics recommend reverse stress testing as an essential supplement to forward-looking regulatory scenarios for both exam and real-world practice.

Recommended

Copyright © Green Risk Education 2026