ESG Frameworks Explained: Essential Guide for Climate Risk Exams

A company can disclose volumes of sustainability data, earn a top-tier ESG rating, and still fall short on real environmental or social outcomes. This disconnect is not a flaw in the system, but it is a reality that high-disclosure firms sometimes score better in ratings despite poor actual performance. For professionals preparing for the GARP Sustainability and Climate Risk (SCR) exam or the CFA Institute’s ESG Investing (SIC) exam, understanding how ESG frameworks and ratings actually operate is not optional. It is the foundation of credible climate risk analysis and exam success.

Table of Contents

- What are ESG frameworks and why do they matter?

- A closer look: Comparing leading ESG frameworks

- Understanding ESG ratings: Why do scores diverge?

- Practical challenges: Benchmarking, costs, and multi-framework reporting

- A practitioner’s perspective: What most exam candidates miss about ESG frameworks

- Take your ESG expertise further

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Frameworks serve unique roles | GRI, SASB, and TCFD each target different aspects, so understand their scope for exam and practical use. |

| Ratings can conflict | Different rating providers use varying methods, resulting in divergent scores for the same company. |

| Compliance costs are substantial | Multi-framework reporting can sharply increase compliance costs, impacting organizational strategy. |

| Efficient data integration matters | Combining reporting frameworks with consistent data infrastructure streamlines compliance and performance. |

| Context justifies framework choice | For both exams and real-world analysis, always match framework selection to business and regulatory context. |

What are ESG frameworks and why do they matter?

ESG frameworks are structured systems that guide organizations in identifying, measuring, and reporting on Environmental, Social, and Governance (ESG) factors. They provide the language, metrics, and methodologies that investors, regulators, and risk professionals use to evaluate corporate sustainability performance. Without frameworks, ESG data would be inconsistent, incomparable, and unreliable for decision-making.

Three frameworks dominate the exam landscape and professional practice:

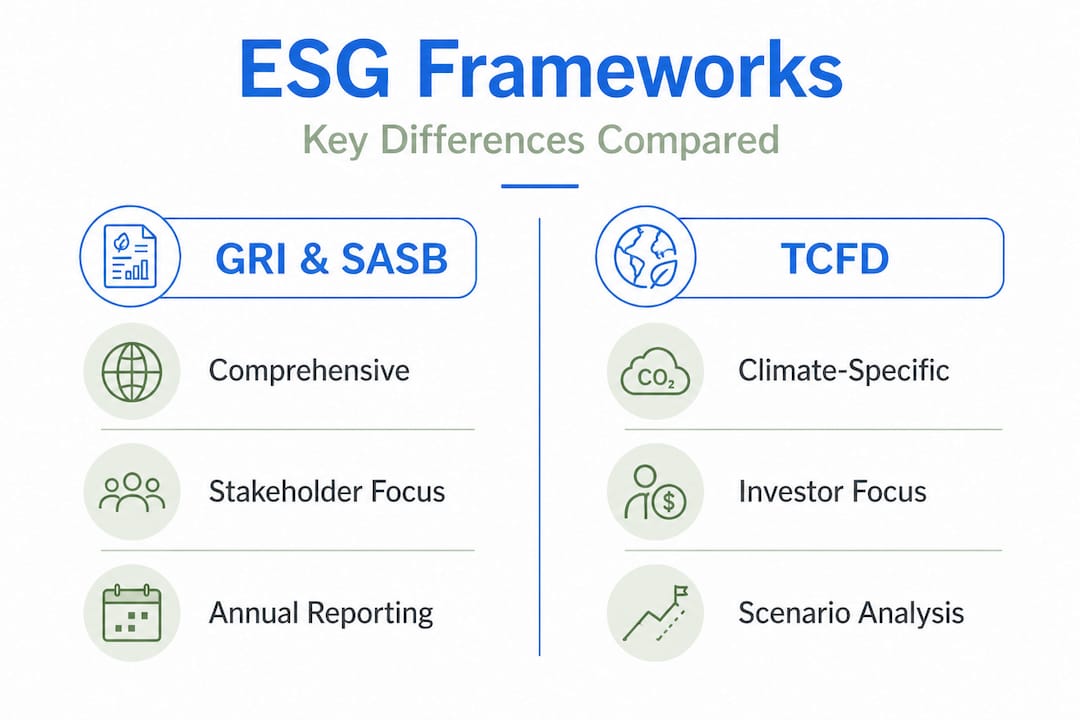

- GRI (Global Reporting Initiative): Focuses on how a company’s activities impact the external world, covering society, the environment, and the economy. It is an externality-focused standard, designed primarily for stakeholder communication.

- SASB (Sustainability Accounting Standards Board): Designed to identify sustainability issues that are material to financial performance. SASB is industry-specific, making it especially useful for investors comparing companies within the same sector.

- TCFD (Task Force on Climate-related Financial Disclosures): Requires organizations to analyze and disclose physical and transition climate risks through scenario analysis. TCFD is structured around four pillars: governance, strategy, risk management, and metrics and targets.

As clearly established in the ESG reporting literature, GRI measures company impacts on society and the environment, SASB measures sustainability issues impacting financial performance, and TCFD requires physical and transition risk scenario analysis for climate resilience. Each framework serves a distinct purpose, and they are frequently used in combination.

For exam candidates, the distinction matters considerably. An exam scenario might ask professionals to recommend an appropriate framework for a pension fund assessing portfolio-level climate risk. That calls for TCFD. A question about comparing carbon footprints across energy companies likely points to GRI. A financial materiality analysis within a single sector points directly to SASB.

“The choice of ESG framework is not neutral. Each framework reflects a different theory of value and a different view of who the primary audience is. Getting this wrong in a risk analysis has real consequences.”

Pro Tip: When approaching a scenario-based exam question, identify the primary audience first. Investors focused on financial materiality? Think SASB. Stakeholders concerned about broader impact? Think GRI. Regulators or lenders assessing climate resilience? Think TCFD. This approach consistently clarifies framework selection under exam pressure.

Professionals can deepen their understanding of key ESG frameworks before sitting for either exam, as these distinctions appear consistently across both syllabi.

A closer look: Comparing leading ESG frameworks

To make the differences concrete, the following table maps each framework by its primary focus, intended user, and reporting type.

| Framework | Primary focus | Primary user | Reporting type |

|---|---|---|---|

| GRI | Societal and environmental impact | Broad stakeholders | Voluntary, impact-oriented |

| SASB | Financial materiality | Investors, analysts | Voluntary, financially material |

| TCFD | Climate-related financial risk | Investors, regulators, lenders | Recommended, increasingly mandatory |

| ISSB (IFRS S1/S2) | Enterprise value and disclosure | Capital markets globally | Mandatory in adopting jurisdictions |

The ISSB (International Sustainability Standards Board) is increasingly referenced alongside the other three, especially in jurisdictions where its standards are being adopted into regulation. For exam purposes, understanding how climate risk strategies connect to each framework is valuable, particularly as the TCFD recommendations have been absorbed into the ISSB’s IFRS S2 standard.

Key distinctions for exam and risk analysis purposes:

- GRI is the broadest, covering 34 topic-specific standards. Its strength is stakeholder breadth. Its limitation is that it does not prioritize financial materiality, which can create noise for investors.

- SASB narrows the scope to what is financially relevant per industry. Its 77 industry-specific standards allow meaningful peer comparisons, but it requires careful sector identification to apply correctly.

- TCFD introduces scenario analysis explicitly, requiring organizations to think about 1.5°C, 2°C, and higher warming pathways. This is directly tested in GARP SCR exam questions on physical and transition risk.

Consider a sample exam-style scenario. A global asset manager wants to evaluate the climate resilience of its real estate portfolio against a 2°C warming scenario. The correct framework is TCFD, not GRI, because TCFD’s scenario analysis requirement is purpose-built for this type of forward-looking, risk-centered assessment. GRI would be appropriate if the manager needed to understand the portfolio’s broader environmental footprint and community impact.

Knowing when to apply each framework, not just what each framework contains, is the skill that separates well-prepared candidates from those who have memorized definitions but struggle with application.

Understanding ESG ratings: Why do scores diverge?

ESG ratings translate framework-based disclosures and other data sources into a single score. They are widely used in portfolio construction, risk screening, and stewardship. But here is what many candidates overlook: two major ratings providers can evaluate the same company and reach dramatically different conclusions.

The reason is methodology. MSCI uses industry-relative performance comparisons on a scale from AAA to CCC, while Sustainalytics measures absolute ESG risk, where a lower score indicates lower risk. These are fundamentally different questions. MSCI asks: “How does this company perform relative to its peers?” Sustainalytics asks: “How much unmanaged ESG risk does this company carry?”

The divergence becomes stark when examining a company like Tesla. Tesla scores highly under MSCI because its electric vehicle products represent strong environmental performance relative to traditional automakers. However, Sustainalytics assigns it a weaker score because of governance concerns and labor-related controversies that carry material absolute risk. Same company, same reporting period, very different conclusions.

| Company | MSCI ESG rating | Sustainalytics ESG risk score | Primary divergence factor |

|---|---|---|---|

| Tesla | AA (Leader) | Medium Risk (24+) | Product vs. governance focus |

| Large bank | A (Average) | High Risk (30+) | Sector exposure weighting |

| Energy major | BBB | Low Risk (18) | Absolute emissions vs. peer ranking |

This divergence has real consequences. It creates challenges in benchmarking, because high-disclosure firms can score well despite weak performance, while low-disclosure firms may be penalized regardless of actual sustainability outcomes. For exam candidates, this is critical to understand, as questions may present a scenario where two ratings conflict and ask for an explanation or a recommended response.

For portfolio professionals, understanding MSCI and Sustainalytics ratings as complementary rather than interchangeable tools leads to more defensible investment decisions and risk analysis.

Pro Tip: Always identify the rating methodology before interpreting any ESG score. An industry-relative rating tells you about competitive positioning. An absolute risk rating tells you about exposure to unmanaged ESG risk. Conflating the two is a common source of error in both exams and professional practice.

Additional factors that drive divergence include scope of coverage (which ESG dimensions are included), data sources (company-disclosed vs. third-party estimated), and weighting of individual indicators. Some providers weight governance heavily; others treat it as a smaller component. These choices compound to produce very different outputs from similar inputs.

Practical challenges: Benchmarking, costs, and multi-framework reporting

Even professionals who understand frameworks and ratings face operational barriers in practice. Three challenges are particularly relevant for both exam candidates and practitioners.

Physical risk benchmarking dispersion. A GARP-commissioned benchmarking study of 13 physical risk vendors found high dispersion in hazard and damage estimates, with flood risk models varying substantially depending on the data source and modeling assumptions used. This is not a minor technical detail. It means that two risk analysts assessing the same asset portfolio using different vendors could reach materially different conclusions about physical climate exposure, necessitating robust model risk management (MRM) frameworks to govern vendor selection and model validation.

Compliance costs for multi-framework reporting. CSRD compliance costs range from EUR 800,000 to EUR 1.8 million in the first year for large companies. Organizations reporting across multiple frameworks simultaneously face compliance costs 40 to 60 percent higher than those reporting under a single framework. This is a direct exam relevance point: candidates are expected to understand the regulatory burden of multi-framework reporting and its implications for corporate strategy and disclosure choices.

“The cost of multi-framework reporting is not just financial. It is also a data governance challenge that most organizations underestimate until they are already committed to compliance.”

Best practices for efficient reporting. Practical guidance points toward a unified data infrastructure as the most efficient path forward.

Steps for effective multi-framework compliance:

- Conduct a materiality assessment to map which frameworks apply to your organization’s activities and stakeholders.

- Build a centralized ESG data repository that captures underlying data points once and maps them to multiple framework requirements.

- Establish data governance policies covering source validation, update frequency, and audit trails.

- Use gap analysis to identify where existing disclosures satisfy multiple frameworks simultaneously (for example, many TCFD requirements align with ISSB S2 disclosures).

- Engage third-party assurance providers early to ensure data quality meets regulatory and investor expectations.

- Train internal reporting teams on framework-specific requirements to reduce errors and rework.

Professionals navigating climate risk disclosure obligations benefit from understanding how these steps reduce both cost and reporting inconsistency. For firms evaluating reporting solutions to manage the operational complexity, purpose-built ESG software increasingly supports multi-framework mapping within a single platform.

The Russell 1000 Blossom ESG index offers a practical illustration: only 431 of the 1,006 Russell 1000 constituents meet an ESG score threshold of 3.3 or higher, underscoring how many large companies still fall short of meaningful ESG performance standards even when data availability is not the constraint.

A practitioner’s perspective: What most exam candidates miss about ESG frameworks

There is a persistent gap between candidates who know ESG frameworks and those who understand them. The former can define GRI, SASB, and TCFD on demand. The latter can explain why a company might score differently across providers, which framework to recommend given a specific business context, and why disclosure quality does not always reflect actual sustainability performance.

This distinction matters more than most candidates realize. Exam scenario questions are designed precisely to probe this deeper layer of understanding. A multiple-choice question might describe a manufacturing company reporting under GRI while claiming TCFD alignment, then ask what critical gap exists in their disclosure. Getting that right requires knowing not just what each framework covers, but where the boundaries are and how organizations sometimes conflate them.

The concept of practical ESG strategies extends beyond reporting to portfolio construction and investment decision-making. Understanding why ESG scores diverge, and being able to communicate that reasoning clearly, positions professionals as credible analysts rather than passive consumers of third-party ratings.

Another underappreciated insight: multi-framework and data consistency challenges are not just operational headaches. They are sources of analytical risk. A portfolio manager who aggregates ESG scores across providers without accounting for methodological differences is building a risk model on unstable ground. Exam candidates who can articulate this point are demonstrating a level of critical thinking that goes beyond textbook preparation.

The actionable recommendation for exam preparation: spend time on edge cases. Practice questions that involve conflicting ratings, incomplete disclosures, or scenarios where the intuitive framework choice is actually less appropriate than a less obvious alternative. These are the questions that separate candidates in the upper score bands.

Take your ESG expertise further

Mastering ESG frameworks and ratings requires more than reading definitions. It demands structured, exam-aligned practice that builds analytical confidence across real-world scenarios.

Green Risk Education offers syllabus-aligned GARP SCR & CFA ESG courses designed by industry experts, covering everything from TCFD scenario analysis to ESG ratings methodology. Candidates can also explore detailed guidance on ESG standards to reinforce framework distinctions and access free GARP SCR notes to accelerate early-stage preparation. Each resource is built to mirror real exam standards, so professionals spend their study time on what actually moves the needle.

Frequently asked questions

Which ESG framework is most important for GARP SCR and CFA ESG exams?

TCFD, GRI, and SASB all appear across both exams, but TCFD’s scenario analysis requirements make it especially central to climate risk modeling questions in the GARP SCR exam.

Why do two ESG ratings for the same company often disagree?

Different providers use fundamentally different methodologies: MSCI uses industry-relative performance comparisons, while Sustainalytics measures absolute ESG risk, so identical companies yield divergent scores depending on the lens applied.

What is the biggest compliance challenge with multi-framework ESG reporting?

Beyond the direct financial burden, with multi-framework reporting costing 40 to 60 percent more than single-framework approaches, maintaining data consistency and auditability across frameworks is the most operationally demanding challenge for most organizations.

How do physical risk benchmarks affect ESG risk management?

Because 13 physical risk vendors show high dispersion in hazard and damage estimates, organizations must implement model risk management frameworks to govern how physical risk models are selected, validated, and compared across providers.

Recommended

Copyright © Green Risk Education 2026